Residence Index UK - Where to Find Yield in 2026

Where to Find Yield in 2026: Beyond London & BTL

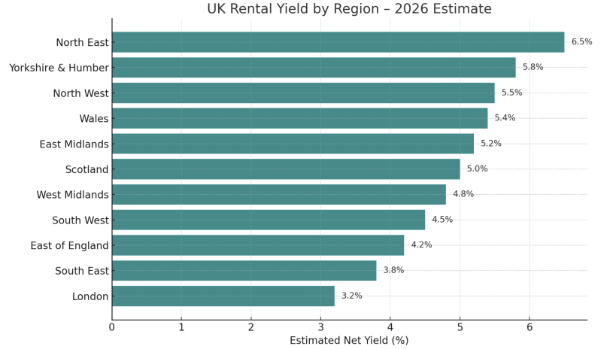

📊 Sources:

🏙️ Major Rental Cities: What You Need to Know

London

- High barriers to entry, low net yield

- Strong long-term capital base but poor cashflow unless leveraged

- Yield play exists in Zones 4–6 or non-prime boroughs (e.g. Barking, Hayes)

- Net yield: 2.5–4%, depending on area and stock quality

Birmingham

- Strong rental demand and regional employment base

- Good mix of young professionals and students

- Core city centre now saturated — value lies in Edgbaston, Perry Barr, outer zones

- Net yield: 4.5–5.5%

Manchester

- Similar to Birmingham, but more BTR dominance

- Shared housing under pressure due to Article 4 and licensing

- Flats near Salford Quays still perform if priced right

- Net yield: 4–5%, unless HMO or PBSA

Liverpool

- Very strong gross yields on low entry prices

- PBSA-led city with high student volume

- Caution on location quality and resale value

- Net yield: 5–7%, higher for cash buyers or SPV PBSA investors

Glasgow

- High rental demand but intense local licensing

- Entry pricing higher than North England but stable

- Net yield: 4.5–5.5%, especially on modern or managed stock

Edinburgh

- Consistently strong rental growth

- Capital value risk is lower, but regulation is rising

- Net yield: 4.5–5% typical (lower on city centre stock)

📍 Where Else to Look in 2026: Hidden Yield Gems

Sunderland

- Gross yields of 7–8% still possible

- Low capital value; high cashflow for BTL or student

- Decent-quality local agents available

Stoke-on-Trent

- Affordable homes, low licensing burden

- HMO and PBSA crossover city with mid-tier unis

- Potential for conversion to 3–4 bed professional or student lets

Hull

- One of the UK’s cheapest entry markets

- Yields of 8–9% possible if well managed

- Strong rental demand but requires agent oversight

Source Notes:

Yield estimates reflect typical net returns after management costs, voids, and basic compliance allowances. Based on data from HomeLet (Oct 2025), Zoopla UK Rental Market Report (Autumn 2025), NRLA yield insights, ONS PRPI, and RIUK internal modelling.

📊 Data current as of Q4 2025. Assumes tenanted, compliant, well-managed stock. For indicative use only – actual returns may vary by property, operator, and local licensing.

🏚️ Yield Risk in 2026: Rent Reform, Turnover & Compliance

The new Tenant Rights Law (2025) adds friction to the traditional BTL model:

- ❌ No Section 21 (all evictions via Section 8)

- 🔁 Tenants can leave after 2 months (periodic default)

- 📈 Rent caps — max one increase per year

- 🏚 Decent Homes Standard = compliance costs

These changes make tenant churn, agent performance, and asset selection more important than ever.